Promissory Note California PDF Template

Stop searching and find out why people love the ease of creating beautiful and legally compliant Promissory Note California PDF with PDFSimpli.

Stop searching and find out why people love the ease of creating beautiful and legally compliant Promissory Note California PDF with PDFSimpli.

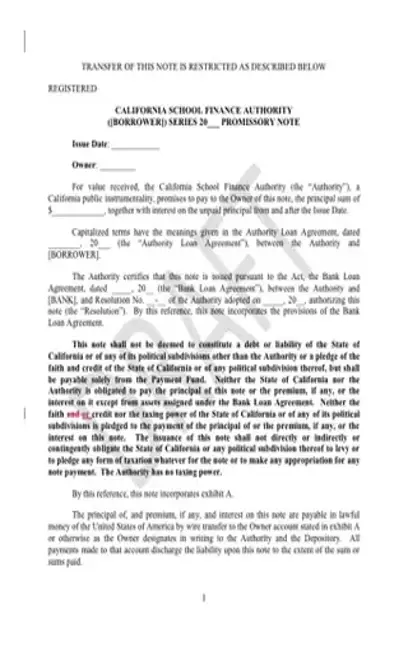

[toc] In the state of California, a promissory note is a type of document that establishes in writing the proposed payback structure of a loan. The document explains the sum of the loan, the amount of interest being paid, and the plan for monthly payments. Promissory notes can be created using a basic template.

Promissory notes are commonly used in California. When two parties negotiate a loan, there needs to be a plan to pay back that loan. A promissory note is a way of getting that payment plan on paper. Both parties are involved in the drafting and signing of the loan, which then serves as a legal contract. Should any issues regarding payment arise, this note is the first legal reference for the situation.

There are two types of promissory notes: secured and unsecured. A secured promissory note involves money that has been loaned between two involved parties, but it’s also used as a security measure for the lender. If a secured promissory note is used, it will contain the relevant loan and payment information, but it will also explain that the lender is entitled to a particular asset if the borrower fails to pay. This asset might include vehicles, a home, land, or any other personal property the borrower owns.

An unsecured promissory note comes with more risk. Because there is not a secured asset involved, the lender doesn’t have a guarantee that they’ll get their money back should their borrower default. As such, most people won’t give unsecured loans to anybody who doesn’t have a good credit history.

There are two main parties involved in the drafting and signing of a promissory note: the borrower and the lender. The borrower is the one receiving the money, while the lender is the one giving it. Unlike a loan agreement, however, only the borrower is required to sign the promissory note. With a loan agreement, both parties would sign the document to show they’d both agreed to the terms.

Promissory notes can be used in lieu of loan agreements between two parties. The circumstances in which a promissory note should be used will vary depending on the type of loan, the relationship of the parties, and the repayment structure.

There are some small differences between a promissory note and a loan agreement. The most important one is that a loan agreement is a great deal more regimented regarding the terms of the payment plan. There are more stipulations in place should the borrower fail to repay. Meanwhile, the promissory note has simple terms that outline simple payment structures. As such, it’s best for simple loans with fixed monthly payment plans.

If one party lends a sum of money to another party, there are two official ways to document the payment plan: a loan agreement or a promissory note.

Loan agreements are the most common form of payment plan. They require the signature of both the lender and the borrower. These contracts tend to be negotiated by attorneys for both parties because of their complexity and legal jargon.

A promissory note is a simpler means of writing the payment plan. If a loan agreement is used instead of a promissory note, the lender and borrower should be prepared to discuss the technical legal terms of repayment.

If the parties use neither a loan agreement nor a promissory note, the lender is at an increased risk. There’s no signed documentation to prove that the lender intended to be repaid. Alternatively, there’s no signed documentation stating the period of time over which the borrower would repay them. This can result in the lender demanding the borrower repay in unreasonably short time periods, or in the borrower failing to pay at all.

When a loan is given, it’s best to have some form of physical documentation. This way, both parties are on the same page, everyone understands their rights, and there’s a reference point should any payment disputes arise in the future. [pdf-embedder url=”https://cdn-prod-pdfsimpli-wpcontent.azureedge.net/pdfseoforms/pdf-20180219t134432z-001/pdf/promissory-note-california.pdf”]

First, take down the addresses of both parties, the balance owed, and the interest rate.

Choose the way you want the balance to be paid. Options include interest-only payments, no installments, and installments. If installments are used, write what time span occurs between each installment.

Write the date at which the full balance is due.

Write the costs of potential late fees along with the time period that must pass before a late fee can be issued. After that, write how many days there are until late fees accelerate.

Get signatures from a witness, the lender, and the borrower.

This depends on if the loan was secured or unsecured. If the borrower defaults on a secured loan, the lender can repossess the unpaid asset. Oftentimes, this is a car or home. If the loan was unsecured, the lender must go through more complex legal channels.

Both types of agreement will work for different situations. What’s important is that you choose one or the other, so that your loan and repayment plan are set in writing.

For the most part, you should register a promissory note with the SEC along with the state of California. Some promissory notes, including ones with terms shorter than nine months, might be exempt from registration. You should double check your legal requirements based on the specifics of the loan.

Select Language

© 2026 , WorkSimpli Software, LLC. All rights reserved.