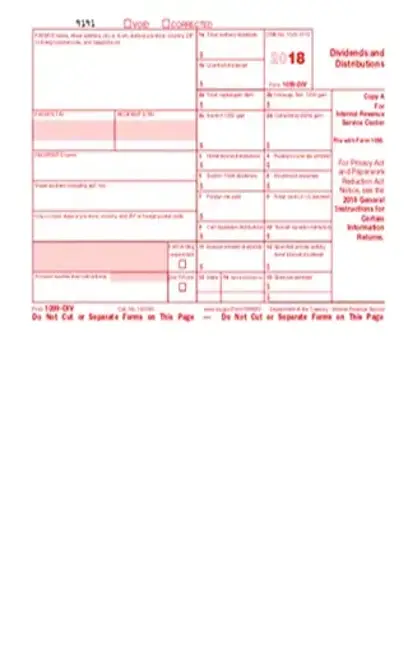

You won’t be the one filling out the form, but this is how to read it:

In Box 1a, you’ll see the total amount from any ordinary dividends you’ve received. Box 1b reflects a portion of Box 1a, showing the dividends that are considered “qualified.” You’ll see mutual fund investment payments listed in Box 2a, while stock market gains will be found in Box 1a.

If your distributions have already had federal and state taxes withheld, the tax amounts will be recorded in boxes 4 and 14. Box 4 is your federal withholding total, while Box 14 is your state withholding total.

Subtract Box 1b from Box 1a to find your non-qualified ordinary dividends. On this amount, you’ll pay a normal tax rate.

Meanwhile, your qualified dividends are defined as a long-term capital gain. If you have a maximum tax bracket of less than 16 percent, these dividends are free of taxes. If you pay a tax rate higher than 15%, the qualified dividends tax rate will be 15% or 20%, depending on your total income.

Dividends are considered “qualified” when they’re paid by United States corporations, or by foreign corporations with a tax treaty with the United States. Stocks must have been traded with the United States stock market, and you must have owned the shares for at least 60 days.

Mutual funds gains, reported in Box 2a, are usually defined as long-term capital gains. This means that the same tax rules that apply to your dividends also apply to your mutual fund gains, no matter whether you’ve had the investment for a week or ten years.[pdf-embedder url=”https://cdn-prod-pdfsimpli-wpcontent.azureedge.net/pdfseoforms/pdf-20180219t134432z-001/pdf/irs-form-1099-dividend.pdf”]