HUD 1 PDF Template

Stop searching and find out why people love the ease of creating beautiful and legally compliant HUD 1 PDF with PDFSimpli.

Stop searching and find out why people love the ease of creating beautiful and legally compliant HUD 1 PDF with PDFSimpli.

[toc] An HUD-1 form is also called a settlement statement form. It’s a standard real estate form put out by the government. In the past, it was used by the closing agent to itemize any charges that were imposed upon sellers and borrowers during real estate transactions. In today’s world, the form is not usually used unless one exception is met.

This document is one that the United States Department of Housing and Urban Development put together. The original intent was for every party involved in a real estate transaction to be given a list of both outgoing and incoming funds. The HUD form also included any transaction fees that had been paid before the closing. These fees would receive a “POC” marking, meaning “Paid Outside of Closing.”

Even though the document is no longer used for every real estate transaction, there is still one main use for it. Reverse mortgages use the HUD form. This is a type of mortgage that’s typically taken out by a seller who is close to or past retirement age. The mortgage is a way for them to pull out their equity. Before 2015, in the period lasting 3 to 10 years after a short sale, lenders would often seek a copy of this form so they had proof of the exact date that the closing occurred.

Also prior to 2015, the federal guidelines and regulations said that borrowers were meant to receive a copy of the form at least one day before the settlement occurred. Some entries would be filed just a few hours before the closing happened. The majority of sellers and buyers would study the statement by themselves, then with their real estate and settlement agents. The more people who reviewed it, the lower the chances of errors occurring.

In its original conception, the HUD-1 form was designed to be used by sellers and buyers of real estate. It was a way of organizing and itemizing all the relevant fees, including fees that had already been paid. After 2015, this is no longer the main statement for organization. However, people with reverse mortgages still use the form.

Nowadays, the form doesn’t need to be used in every real estate transaction. Instead, it should be used when a person sets up a reverse mortgage. Reverse mortgages are designed to let homeowners borrow equity. Rather than making payments to their lender, their lender will make payments to them. Payments might be a lump sum, periodic advances, monthly payments, or any combination of these things.

You can qualify for reverse mortgages if you’re over 62 years old and you have an adequate amount of equity in your home.

This is the main way to record and itemize your transactions when a reverse mortgage is involved. It’s important that all information be reflected and updated as accurately as possible. Multiple people should go over the form to make sure that all of the numbers are correct. It’s common for little mistakes to show up on the form, and these little mistakes can have a big impact down the road.

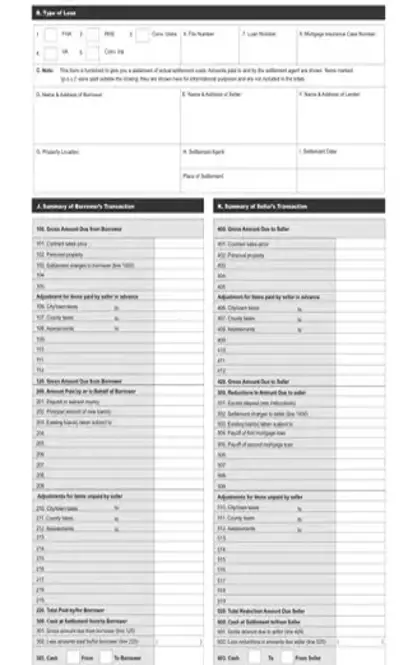

In Part B, you’ll have to give details about the type of loan you’re financing. You will have to check the relevant box. In Question 6, you’ll give your case file number, and in Question 7, you’ll give your official loan number. If you have a mortgage insurance case number, you’ll provide that for Question 8.

Part D will capture the borrower’s name and current physical address. Part E does the same for the seller. The lender’s name and physical address are captured in Part F. Part G is designated for the location of the property; you should put the real estate’s physical address here. In Part H, you’ll write the name of the settlement agent and the place that the settlement occurred. Part I will reflect the settlement date.

Part J will ask for the summary of the borrower’s entire transaction. This is where you’ll record all relevant fees and other miscellaneous transaction data. You’ll give the sales price of the contract, the price of personal property, and any settlement charges given to the borrower. If there’s an adjustment for any items that the seller paid for, you’ll note it here as well. Give information about the loan, taxes, and any adjustments made for these things.

In Part K, the seller will make a similar list of their transactions. It will include any settlement charges to them, any existing loans, and when the first or second mortgage loans were paid off.

Part L will note the total settlement charges. This is where the total amount of fees for the real estate broker are recorded, along with items payable and items required to receive advance payment. If the lender has any reserves deposited, or the transaction included title charges, they should be listed here as well.

The final part of the form is an outline of the loan terms. This is where the person will write their initial loan amount, the amount of years that the loan term lasts, and the initial interest rate. You’ll make notes of whether the interest rate is capable of rising, if the loan balance can rise, and if there are any prepayment penalties. All of these details should be worked out between the buyer, the seller, and the lender.

If you use this form, copies of it should be given to all parties involved in the transaction. This includes the agents, lender, buyer, and seller.

As of 2015, all real estate transactions were no longer required to use this form. The new form is referred to as a Closing Disclosure form.

A closing disclosure is required to be filed with any real estate transaction. It is basically the same as a person’s closing statement.

Select Language

© 2026 , WorkSimpli Software, LLC. All rights reserved.