Personal Balance Sheet Template

Stop searching and find out why people love the ease of creating beautiful and legally compliant Personal Balance Sheet with PDFSimpli.

Stop searching and find out why people love the ease of creating beautiful and legally compliant Personal Balance Sheet with PDFSimpli.

[toc] It’s common for people to check their bank and credit card statements, only to be surprised by the amount of money they’ve spent. Financial accountability is important, especially if you want to build your credit and stay up-to-date on bills. One way of keeping a record of your expenditures and income is to use personal financial statements. A personal balance sheet template is one format for personal financial statements. This Statement will detail your assets and liabilities and serves as a sheet for your net worth calculation. You will include your assets such as cash, savings account balance, bank account checking balance, money owed to you, retirement funds or investment, etc. You will take into account liabilities the following: debt from loans, long-term debt, short-term debt, short-term loans, personal loans, income taxes owed, student loans, credit card debt, contingent liabilities, mortgage, and car loan. Use PDFSimpli to Edit and fill your Personal Balance Sheet Form with this user-friendly editor.

You would use a personal balance sheet to keep track of your spending and income. The main goal of a balance sheet is to show you an overall look at your wealth during a specific time period. The sheet will summarize your assets, your liabilities, and your overall net worth.

Your assets are the things you own, including your money itself, your house, your car, and other items. Your liabilities refer to things you owe, like lease payments and utility bills. To calculate your net worth, you subtract your liabilities from your total number of assets.

Personal balance sheets can be used by anyone who wants a comprehensive look at their finances. It doesn’t matter whether you’re a wealthy business owner or a struggling minimum wage worker. The sheet will help you get all of your financial information on paper. Once you have this information, you can make decisions about your financial future.

You might find that you’re spending too much in one area of your life, or that impulse spending is having a marked impact on your finances. By using a personal balance sheet, you can get a sense of what your income is, what your expenses are, and what your budget is relevant to that.

For people with a little extra money on hand, the personal balance sheet can also be used to give you a sense of what investment opportunities you might want.

A personal balance sheet is ideal for anyone who wants to get their finances in order. Even if you’re confident in your monthly budget, it still helps to use a balance sheet. Doing so gives you a visual representation of your cash flow for the month. If you fill out a sheet each month, you can get a sense of where you should be budgeting more tightly. Alternatively, you might also see places where you could be spending more.

Personal balance sheets are extremely helpful if you’re planning on making any new investments. If you intend to move into a bigger place, for example, you’ll want to be sure you can handle the increased rent. If you want to buy a house, you’ll need to make sure you have enough money to handle the down payment. The same is true if you want to purchase a car.

Personal balance sheets aren’t legally binding forms or contracts. You won’t run into any legal problems if you don’t have one, and you won’t lose any work or housing opportunities. But if you don’t have a personal balance sheet, you’re more likely to struggle with your budgeting and spending. This is especially true if you don’t have an on-paper budget drawn up, either.

Ultimately, a personal balance sheet is a tool that you can use to benefit yourself. It will help you stay organized from month to month. You’ll be able to keep track of your net worth, expenses, and income. If adjustments need to be made, the balance sheet will show you where the problem areas are. These sheets also make drafting on-paper budgets and financial plans much easier.

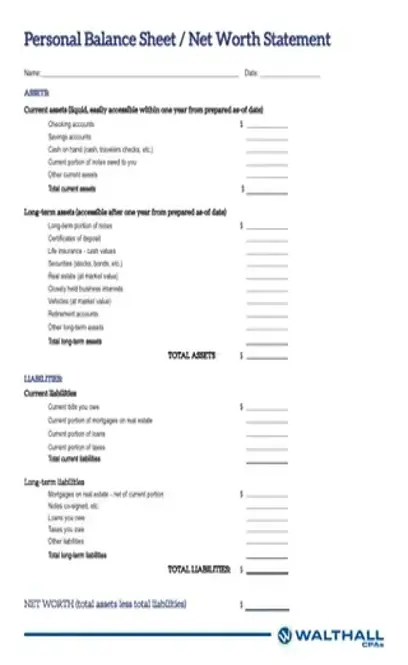

There are three distinct parts of the personal balance sheet: your assets, your liabilities, and your net worth. You should calculate your assets first. Assets come in three different categories:

Liquid assets – These assets are things that you can easily sell for cash without a loss in value. You’d include cash, money market accounts, savings accounts, and checking accounts.

Large assets – These are the expensive physical things you own. You’d include any cars, boats, houses, furniture, and artwork in this category. Your personal balance sheet should reflect your items’ market value. When you can’t find the market value, you can use the recent sale prices of comparative items.

Investments – Your investments include real estate, mutual funds, certificates of deposit, stocks, and bonds. All investments should be recorded based on their current value on the market.

Your liabilities are the things you owe. The following expenses would be part of your liability listings:

Current monthly bills

Recurring monthly expenses

Continuing payments on your car or house

Unpaid credit card balances

Other loans

Your net worth reflects the difference between the number of things you own versus the number of things you owe. This figure represents your true wealth, as it reflects how much money you have once all of your liabilities have been paid. If you discover you have a negative net worth, this means that you currently owe more money than you own.

To calculate your net worth, you should first total everything in the “Assets” column. Then, total everything in the “Liabilities” column. Subtract the liabilities total from the assets total. The remaining figure is your current net worth.

If you fill out a personal balance sheet each month, you can keep track of your increasing net worth. Net worth can be increased by paying off your liabilities or increasing your number of assets.

There are! Most people use a personal balance sheet in conjunction with a cash flow statement. The cash flow statement will tell you exactly where your cash is coming from and where it’s going. Meanwhile, your personal balance sheet will provide a snapshot of your total wealth at any given point in time.

Most people create monthly, quarterly, and annual balance sheets.

Personal financial statements are a way to reflect and manage your personal wealth. A balance sheet is a type of personal financial statement.

Select Language

© 2026 , WorkSimpli Software, LLC. All rights reserved.